Stablecoin Banking Rails.

nupont connects the banking infrastructure you already operate to public stablecoin rails — faster settlement, freed liquidity, and full regulatory compliance. Without changing your core systems.

Three outcomes your treasury will recognize.

30 sec

Speed

Settlement at on-chain finality — around 30 seconds, 24/7. No cut-off times, no weekends, no correspondent delays.

3–5 days today → seconds on rail

€7M+

Liquidity

No capital permanently tied up in pre-funded Nostro accounts. Your USDC buffer turns over with each payment — not parked for days.

Pre-funded Nostros → just-in-time funding

-70%

Cost

No correspondent fees, no lifting fees, no FX margin stack across multiple hops. The bank captures the corridor margin instead of relaying it.

Multiple fee layers → single network fee + nupont

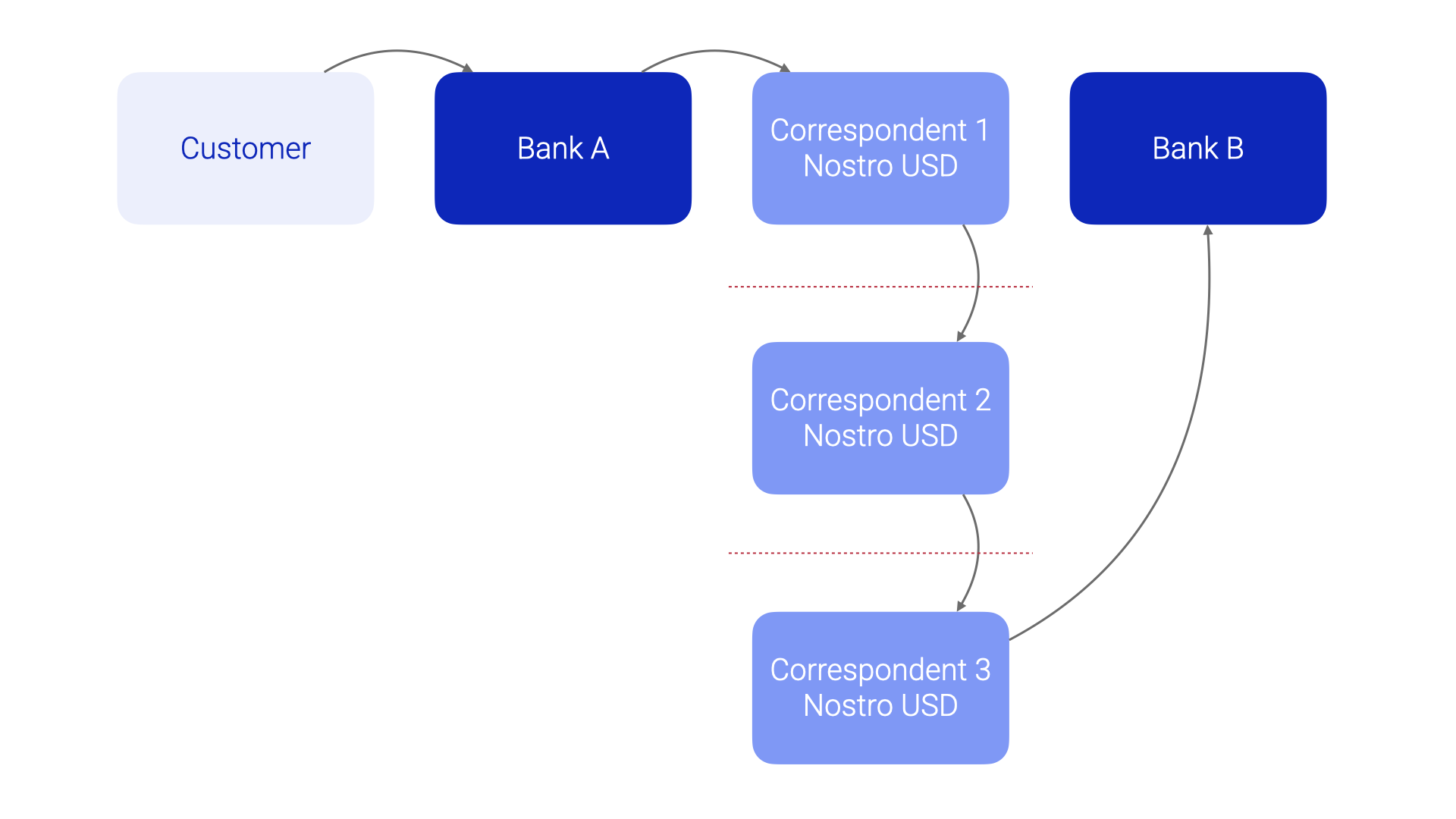

Cross-border payments still cost your bank capital, time and margin.

A single corporate USD payment from Germany still travels through multiple correspondent banks, parks seven-figure capital in Nostro accounts that earn nothing, and takes 3–5 days to settle. Your customer has no visibility. Your treasury carries the cost.

3–5 days end-to-end for a single correspondent payment

Multiple fee layers across correspondents, FX desks and lifting fees

Millions tied up in pre-funded Nostro accounts per corridor

Weekends and holidays lock your customer out of the rail entirely

One rail. Settlement and messaging atomic.

nupont collapses the correspondent chain. The same pacs.008 your bank sends today — but the value moves on a public stablecoin rail in seconds, not through a chain of intermediaries.

Your bank retains the full customer relationship. nupont provides the technical infrastructure behind the scenes.

Same ISO 20022 formats your operations team already uses

Electronic banking frontend unchanged

Customer sends pain.001 or utilizes online banking

Settlement finality in seconds, not days

Account statements delivered as camt.054 and camt.053 — straight into core banking

Four steps. Standards in, standards out.

Step 1 — Payment originates at the bank Your customer instructs a USD payment in the electronic banking frontend. FX (EUR → USD) is booked before the bank forwards a standard pacs.008 to nupont via webhook. Nothing changes on your side.

pacs.008 · USD

Step 2 — nupont prepares the on-chain transfer nupont resolves the receiving bank's BIC to a USDC wallet address, prepares the transfer and sponsors the gas fee. The bank does not need to hold ETH. The unsigned transaction is queued for the bank's HSM.

ERC-3009 · gas paid by nupont

Step 3 — The bank signs in its own HSM The bank's Hardware Security Module signs the transaction with its own USDC wallet key. Private keys never leave the bank. nupont is technical orchestrators — not custodians, not a CASP.

EIP-712 · key never moves

Step 4 — Statements close the loop nupont's indexer detects the on-chain transfer. An intraday camt.054 is sent immediately to both banks — proof of settlement, in seconds. The camt.053 follows for end-of-day final booking. Standard ISO 20022, straight into your core banking system.

camt.054 intraday · camt.053 end-of-day

ISO 20022 account statements. Patented.

nupont's blockchain indexer monitors every on-chain transfer and translates it into the banking formats your systems already consume. No manual reconciliation, no separate reporting workflow.

Both the sending and receiving bank receive a full statement set for every payment:

camt.054 — intraday status report, fires within seconds of on-chain confirmation

camt.053 — end-of-day final booking statement

Delivery via Queue, EBICS or sFTP

Formats also available: MT940 / MT942 / BAI for crypto account monitoring

The same statement infrastructure that powers cross-border payments also supports your corporate clients who hold their own stablecoin or crypto accounts — giving them a consolidated view of fiat and digital assets through a single banking channel.

MiCAR-compliant. No new crypto or banking licence.

Regulatory clarity was built into the design from the start.

✓ Keys stay at the bank USDC wallet keys live inside the bank's own HSM, signed in-house — never exported. Auditable within your existing key management framework.

✓ nupont is not a custodian nupont never holds, controls or transfers customer assets. We prepare the transaction. The bank executes it by signing.

✓ USDC is a regulated EMT USDC is an Electronic Money Token under MiCAR. Circle is the regulated issuer. The bank is the regulated counterparty. Your existing AML, sanctions and reporting workflows apply unchanged.

✓ Your customer never sees USDC The customer pays EUR. The recipient receives USD. USDC is settlement infrastructure between banks — not a product offered to clients.

Minimal change. Maximum impact.

STAYS UNCHANGED: Core banking system, electronic banking frontend HSM infrastructure ISO 20022 messaging Sanctions screening EBICS / sFTP delivery ERP downstream integration AML and KYC workflows

WHAT'S NEW: One webhook between bank and nupont One USDC wallet key in the bank's HSM One BIC-to-wallet entry per counterparty bank

Empower your clients to manage crypto alongside fiat.

For banks that want to go further — nupont's white-label application gives your corporate clients direct access to their stablecoin and crypto accounts within your own branded interface. View holdings, monitor transactions and receive account statements in one place, seamlessly integrated with your existing banking portal.

Consolidated view of fiat and digital asset accounts

White-label with your bank's branding

API integration for a unified customer experience

Supports non-custodial wallets held by your corporate clients

Account statements via MT940, camt.052, EBICS and sFTP